This issue, we take a closer look at HDB rentals, which have seen volumes pick up in recent quarters, even as rents continue to slump.

By Chang Hui Chew

As we cross Singapore’s 50th anniversary of independence, we look around at our HDB flats, often thought of as a world class public housing programme that has contributed to the dizzy heights of our nation’s success. In 50 years, the HDB flat has become quintessentially Singaporean, and is now the primary source of many Singaporeans’ wealth. Last issue, we looked at the HDB resale market and predicted a recovery where transaction rates would pick up while prices would continue to remain depressed. This issue, we give you the Guru View of HDB flat rentals.

Overall rent and volumes

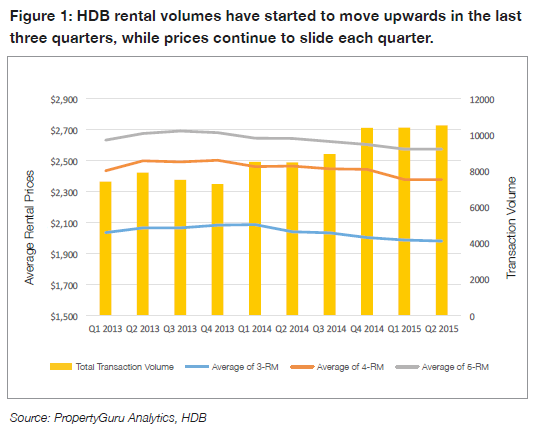

Transaction volumes, reported by HDB as approvals for subletting, have been moving upwards while prices have dipped over the same period (refer to Figure 1), with 3-, 4- and 5-room flats accounting for over 90 percent of the approvals. The private condo market has seen rental volume jump by 21 percent year-on-year in the first half of 2015, while rental prices have seen declines of about 3.9 percent year-on-year over the same period. We see a similar trend observed in the HDB market as well, with rental units continuing to move, while prices dip.

The increase in HDB rental demand is likely due to shrinking expatriate compensation packages as salaries become “localized”. Furthermore, with many multi-national companies moving out of the Central Business District to more suburban locations like Changi and Alexandra Business Parks, rental demand has also followed.

New permanent residents (PRs) are also likely to contribute to the buoyancy of rental volumes as well. New PRs have a mandatory waiting period of three years before they can buy a resale HDB flat off the open market, and will have to rent a flat in the meantime.

As such, older, larger HDB units conveniently located near suburban hubs, public transportation and amenities like supermarkets remain popular with tenants, and will continue to enjoy higher demand. We see this reflected in the price resilience of 5-room rents, with average monthly rents dipping a mild 4.4 percent from its previous peak in Q3 2013. In contrast, 3-room flats saw average monthly rentals fall 5.1 percent over the same period.

It is likely that rental supply is responsible for keeping rental prices down, despite an increased demand and uptake for rental units. In these past few years, a record number of private residential units have been completed, with many HDB upgraders choosing to lease out their existing units, instead of selling them off. With HDB resale prices falling, HDB sellers might prefer to hold on to their units until the property cycle goes back on the upswing, or just hold onto their units for passive income. With increased supply in the market, even with increased demand for rental HDB flats, prices are unlikely to see much upward movement.

Splitting by type

3-room flats have, for the period under analysis, been the bulk of subletting approvals. This is likely due to their lower quantums, making them a popular option for new PRs waiting out their three-year time bar. 3-room flats are also a likely option for newlyweds waiting for their BTOs or condo units to complete, if they choose not to live with their parents.

In recent quarters however, 3-room flats are seeing their lead shrinking, with 4-room flats seeing a sharper 3.4 percent increase over the last quarter (refer to Figure 2). This is in contrast to 3- and 5-room flats which saw minimal gains under 1.0 percent in the same period. Given decreasing monthly rentals, tenants might find that springing for a larger 4-room flat over a 3-room is within their means. We also continue to see differences between mature and non-mature estates, with 5-room flats in mature estates commanding an average premium of 17.4 percent over HDB flats in newer estates.

Prices by estate

More centrally located mature estates saw a larger degree of price movement, quarter to quarter. Queenstown saw a 6.4 percent growth for 4-room flats, while 5-room flats dipped 3.1 percent, between the first and second quarters of 2015. Bukit Merah saw rents for 4-room flats bump 1.7 percent upwards while rents for 5 room flats dipped 0.6 percent over the same period. 3-room flats in the central area saw price dips of 2.1 percent as well.

3-room flats in Kallang / Whampoa saw median monthly rents move up by five percent while 5-room flats fell by the same amount. Rents for 4- and 5-room flats in Toa Payoh fell by 1.9 and 1.7 percent respectively. Marine Parade, perennially popular with expatriates, saw 3- and 4-room median rents remain flat for the first half of the year. The mature estates continue to reflect downward pressures on HDB rental pricing, even if transaction volumes are picking up.

Non-mature estates were more muted in their price movements, with many estates seeing rentals remain flat for the first half of the year. Sengkang saw rental prices of its 5-room and executive flats depress 2.1 percent and four percent respectively, while Woodlands and Yishun also saw their 5-room flats dip by just over four percent. Sembawang saw the sharpest dip of the first half of the year, with executive flats sliding 7.6 percent for the first half of the year.

Looking at demand

The popularity of mature estates bears out in PropertyGuru’s proprietary search data as well. In the second quarter of 2015, the five most searched HDB estates for HDB rentals were Bedok, Yishun, Jurong West, Ang Mo Kio and Tampines (see Table 1). Out of these, HDB considers Bedok, Ang Mo Kio and Tampines mature estates.

Interestingly, Jurong West, even as a far flung non-mature estate, saw median monthly rents in the second quarter on the higher end for each flat type. This is likely due to the higher demand for rental units in the area, due to foreign students at Nanyang Technological University, and foreign workers from the Tuas and Jurong West industrial areas.

Location is also likely to play a big part in these estates popularity with tenants, as three out of the five of the most searched HDB estates for rental – Bedok, Yishun and Ang Mo Kio – are all less than half an hour via the MRT to the Orchard Road shopping belt.

With search demand being a forward indicator of rental transactions, we expect that the rental transactions for these five estates is likely to increase by the end of Q3 2015 as well.

Tenants squeezing hard

With prices dipping, it’s a tenants’ market right now, with many landlords being squeezed for additional perks. Common concessions mentioned by real estate agents include lowered rents, provision of furnishings and shorter lease terms. Tenants also have the leeway to be more selective given the slower market, and can take their time to look for choicer units, such as those closer to public transportation and suburban shopping centres.

For landlords, this means being open to negotiation and compromise. It would ultimately be cheaper for landlords to lose a few thousand in rental income over the course of the lease by bringing rents down a couple of hundred dollars per month, than to have the rental unit lie empty for a few months without generating any rental income.

Landlords could also switch tack by renting out individual rooms instead of the entire unit, which often pushes up yields. However, this increases the hassle as the landlord will be dealing with more than one tenant. Using such a strategy might increase some costs as well, as there will be greater wear and tear on assets in the flat over time.

A quick outlook

The outlook for HDB rentals is similar to that of HDB resale flats. For the next half of the year, we expect HDB rental volumes to continue to increase, especially as businesses decentralize and suburban areas continue to grow as business hubs. The URA Masterplan gives us an idea of what these areas are likely to be:

• Paya Lebar, with the planned commercial area of Paya Lebar Central. The HDB estate of Geylang is poised to capitalize on this area.

• Jurong East, with the Jurong Lake District and Jurong Gateway. Between the planned commercial development and the construction of the Singapore Malaysia High Speed Rail terminus, Jurong East should see HDB rental demand rise even more.

• Changi Business Park, with an expansion of half a million square metres of commercial space and the upcoming Singapore University of Technology and Design. The nearby estates of Simei and Tampines, with convenient transportation links to the area should see rental prices increasing even more over time.

• Jurong West, with JTC’s new CleanTech Park, and the revitalization of industrial areas like Tukang, Tanjong Kling and Wenya. With an increased demand for skilled cleanand high-tech workers, HDB rental demand in Jurong West will continue to increase as well.

Most of these HDB estates are highly developed, with established infrastructure and amenities. This makes them more attractive not only to expatriates moving to Singapore, but to locals as well, who might want to rent units closer to their place of work.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||