Singapore’s luxury residential developments have, despite their increasingly premium prices, proven consistently popular amongst home buyers. But how have the cooling measures implemented in recent years affected the situation? We explore the current market climate.

By Cheryl Marie Tay

Singapore is known worldwide for many things, one of which is its abundance of luxury residences. From condominiums and semi-detached homes to bungalows and even mansions and villas, there is certainly no shortage of upscale housing on this tiny island from which to choose.

Yet in September 2009, thanks to the significant increase in the number of foreigners buying private residential properties in Singapore, the government introduced property cooling measures to avoid a potential housing bubble. Additional taxes were enforced on those buying their second and subsequent homes, and restrictions regarding who could buy what type of residential

property became more stringent.

This led to a price correction across the board in the private residential market, as well as slower buying activity, with the regulations reviewed and revised twice a year since then, all the way till December 2013. Though different segments of the market have been affected to varying degrees, some more than others, the effects of the measures cannot be denied.

Reviewed, revised… but still resilient

Though the aforementioned cooling measures initially caused a fall in private residential property prices, and the measures have not been reviewed since 2013, private home sales have been climbing relatively steadily. Both the Good Class Bungalow (GCB) and luxury apartment segments have performed well, with sales volume recovering from previous dips and stagnation caused by the cooling measures (refer to Figure 1).

Sales push

According to CBRE Research, in the first half of this year, the sales volume of apartments in the Core Central Region (CCR) worth $5 million and above topped that in the second half of 2014 by 45.7 percent (refer to Figure 2). Property developers have been more aggressive in marketing units in their projects, both in Singapore and overseas. This is especially true for projects that were completed within the past 12 to 18 months, with prices ranging from $2,600 psf to $3,000 psf (the latter more common in newer projects).

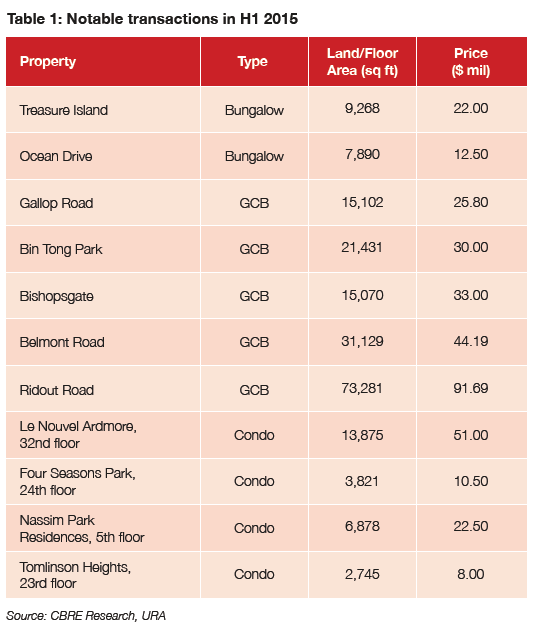

Notably, 16 units at Marina Bay Suites were sold for $2,100 psf to $2,500 psf each, while at Goodwood Residence, 20 units were sold for $4.4 million to $6.6 million each. Furthermore, seven Tomlinson Heights units were sold for $7.6 million to $11 million each, and a penthouse at Le Nouvel Ardmore measuring 13,875 sq ft was sold for the record price of $51 million.

Developers with unsold housing units are expected to continue to actively promote them, and CBRE Research foresees a gradual return of market confidence, as well as minimal downside in prices due to no new luxury supply beyond 2017 having been announced.

Fizzling on the beach

Sentosa Cove, on the other hand, has not enjoyed as good a year so far. Famous for being the prestigious, coveted location of possibly the most pricey landed homes in all of Singapore, and once an enclave for wealthy foreigners to buy luxury residential property here, its housing market has been experiencing a downturn.

When it came to its bungalows, only three transactions took place throughout 2014, and caveats were lodged for just two bungalows in the first half of 2015. CBRE Research attributes this poor sales performance to cooling measures such as the Total Debt Servicing Ratio (TDSR) framework and Additional Buyers’ Stamp Duty (ABSD), imposed on both local and foreign investors.

The two bungalows in question, one on Treasure Island and the other at Ocean Drive, had an average price of $2,011 psf, 20 percent higher than the average $1,676 psf of the three bungalows sold last year, and 5.3 percent lower than the average price in 2013. 2014’s unusually low prices were the result of less attractive property features, such as non-sea facing orientation, alongside smaller land and built-up areas.

Recovery in Sentosa Cove’s bungalow market is expected to be sluggish, in part because of the hurdles it has to overcome, thanks to the property cooling measures. Another reason for its delayed recovery is Singaporeans’ reluctance to invest in residential property in the area, as they are able to purchase freehold bungalows at comparable prices in more convenient and accessible locations in mainland Singapore. Considering all this, sellers would do well to lower their price expectations when negotiating with potential buyers.

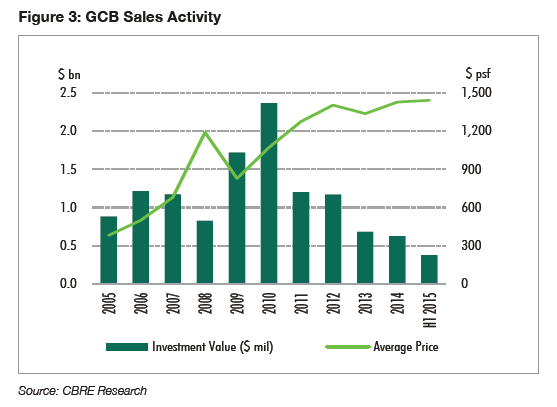

Good class, good sales

The Good Class Bungalow (GCB) segment, on the other hand, has been doing far better than the bungalow market in Sentosa Cove (refer to Figure 3). In the first half of this year alone, 15 GCBs were sold, maintaining the segment’s consistent performance of last year, when 15 GCBs were sold in H1 and 13 were sold in H2.

Of the GCBs sold in H1 this year, seven were smaller bungalows measuring below 15,070 sq ft each in land area. Unsurprisingly, these bungalows were more affordable, each costing between $7 million and $10 million. This is in stark contrast to larger GCBs, which cost more than twice ($20 million to $30 million each). One example of the latter is a 31,129 sq ft GCB on Belmont Road, which was sold for $44.19 million.

Good class investments

Investment-wise, Singapore’s GCB sector displayed significant improvements from last year, registering an investment value of $377.6 million in the first half of this year, 9.8 percent higher than the $344.8 million recorded in the first half of last year and 33.9 percent higher than the $282.06 million recorded in the second half of last year.

This healthy performance in the GCB segment could very well be attributed to the sale of a large 73,281 sq ft GCB on Ridout Road for $91.69 million. Using land area as a guide, the average price of GCBs in the first half of this year was reported as $1,442 psf, lower than H1 2014’s $1,488 psf but higher than H2 2014’s $1,381 psf. These figures show that prices of GCBs have remained at a consistently high level, despite their overall sales volume having shrunk significantly in the past two years.

Positive prediction

At the same time, this also means that though the cooling measures have not managed to adversely affect prices in the GCB market, they have contributed to the more muted buying activity observed in recent years, and have also prevented investors from over-leveraging themselves, mortgage-wise. This has in turn led to a stronger, healthier property market. Additionally, it helps that buyers of GCBs tend to be either owner-occupiers, or long-term investors with a greater pool of finances.

For the second half of this year, CBRE Research predicts that prices will remain resilient, and that another 10 to 15 GCBs will be sold, maintaining the GCB market’s strong performance thus far.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||