Last issue, we gave the GuruView on HDB rentals. This issue, we look at the private residential rental market to understand where the market will be going in the next six months and beyond.

By Chang Hui Chew

The story of the private residential rental market is one that has taken a double whammy over the past few years, with many landlords dealing with falling rents, weak yields and a difficulty in attracting tenants.

On the demand side, a decreasing number of employment passes are being issued, leading to fewer expatriates arriving on our shores. Furthermore, expatriate remuneration packages are being localised, leading to lower budgets to be spent on housing. This applies further pressure on rental prices as well, and shifts demand from centrally located districts such as 9, 10 and 11, to districts further afield.

On the supply side, a record number of residential units have been completed or are due to be completed in 2015 and 2016, before tapering down in 2017. Many of the units due to hit the market include investor favourites such as shoebox, one-bedroom and one-plus study configurations, adding on to stock that is already in the market.

Units rented, units coming

Supply side factors, coupled with weakened demand, is one of the primary reasons why landlords are finding it hard to tenant their units. Stocks of private condos have been on a steady increase in the past two years, and hit just under 250,000 at the end of the second quarter of the year (refer to Figure 1). Current URA estimates indicate that almost 20,000 private residential condo units will be completed by the end of 2016, and another 13,000 by end 2017. This was due to an increase in government land sales between 2011 and the start of 2013, together with aggressive buying by

developers building up their land banks.

At the same time, vacancy rates have also been on an upward trajectory, crossing nine percent at the end of Q4 2014, and again in Q2 2015. Vacancy rate, as defined by the URA, is the percentage of stock units that are not physically occupied. Market watchers have expressed concern that vacancy might hit 10 percent by the end of the year as well. What this means for landlords is a lot more competition for a shrinking tenant pool, putting further pressure on rents.

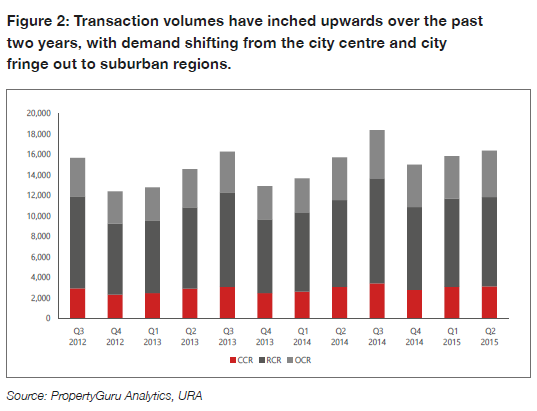

While stock has increased, demand for units has not. Overall private condo transaction volumes between 2013 and 2014 actually increased 11 percent year-on-year, with volumes in the Outside Central Region (OCR) growing by 16 percent over the same period (refer to Figure 2). For 2015, the first half of the year saw just under 8,700 rental contracts reported in the OCR, a 15 percent increase from H1 2014. In contrast, the Core Central Region (CCR) and Rest of Central Region (RCR) saw rental transactions inch upwards by nine and seven percent respectively. This suggests that demand for private condo rentals has not necessarily shrunk yet. Rather, with expatriate housing budgets shrinking, demand is shifting from the city centre and city fringe to suburban regions.

Rental price and yields

With the upcoming increases in stock and shifts in demand, landlords need to price their rentals aggressively in order to tenant them. With current market conditions, rental prices have had to moderate. The URA’s overall Rental Price Index (refer to Figure 3) saw rental prices on an upward climb until it reached a peak around Q3 2013, before it began its decline. Since then, the Index saw an overall decline of about 5.4 percent to its current level of 111.0.

The more price-sensitive OCR, with a much wider variety of competition, was the first to bow to market pressures, with prices starting to fall from Q3 2013, dropping 6.7 percent between its peak and the end of Q2 2015. The CCR held out a little longer but began to see declines from Q1 2014. It also saw the largest percentage tumble at 7.2 percent from its last peak in Q3 2013. The RCR proved more resilient, with prices only seeing declines from Q2 2014 onwards, and a slighter dip at 3.1 percent.

Knight Frank tracks rental prices through a basket of properties, classifying them as high-end, mid tier and mass-market. According to the consultancy’s figures, average rentals for the mass-market fell nine percent, the mid-tier 10 percent and the high-end seven percent between Q2 2013 and Q2 2015 (refer to Figure 4). The mid-tier saw the sharpest drop in actual rental quantum as well, falling $0.50 between Q2 2013 and Q2 2015. This suggests that over the period, landlords of an average sized 800 sq ft apartment would have seen $400 less in rent per month.

While the overall smaller drop in the high-end tier might suggest it is a little more resilient in the medium term, it seems to be more volatile in the short term, with the sharpest decline (2.3 percent) out of all three segments quarter-on-quarter in Q2 2015.

As rental prices fell, gross yields were also hit (refer to Figure 5). Mid-tier and mass-market condos saw rental yields falling to just under 3.6 percent in Q2 2015, according to Knight Frank’s estimates. Gross yields for high-end properties, however, inched upwards 3.2 percent despite falling rental prices, and are doing so for the second consecutive quarter. With gross yields so tight, it is likely landlords will still be required to come up with money out of pocket to foot other costs of ownership.

Without any expected changes to market conditions, rental prices are not expected to see upsides for the rest of the year. Knight Frank predicts that the OCR is likely to see the largest softening in rental prices for the second half of the year, with an estimated 63 percent contribution to the upcoming supply in the latter half of 2015.

This places landlords of newly completed units who do not have adequate holding power and can stomach lower rents in a difficult dilemma. Holding on to their rentals would mean more money out of pocket each month, even with a tenanted unit. However, trying to offload these poor-yielding rental units would not only expose them to the weak private residential resale market, but also subject them to Sellers Stamp Duty (SSD), which could range from four to 16 percent, depending on when they bought the units. Landlords who wish to offload their units will also need to contend with the chilly private residential resale market, and it is unlikely they would be able to sell at a price they might find palatable.

Landlords need to compromise

Given the shrinking tenant market and a glut of rental units on the market, landlords need to realise tenants are in a much better bargaining position. It would therefore be unrealistic for them to hold on to a desired rental price level, or be choosy about their tenants. They would be far better off compromising and accepting a lower offer than leaving the unit untenanted.

The math is simple. Assume that a landlord is currently paying a mortgage of $3,200 a month for a one-bedroom condo unit, and a tenant is offering $2,800. Over the course of a one-year lease, the landlord would have to pay $4,800 out of pocket to make up the difference in the mortgage. However, if the landlord were to leave the unit untenanted for just two months, he or she would already owe $6,400 in mortgage payments out of pocket.

Aside from compromising on rental prices, landlords can also negotiate on other aspects of the rental contract. For instance, landlords can offer to provide furnishing or to offset utilities. They can also consider negotiating for a shorter one-year lease instead, as it provides them the chance to re negotiate terms if market conditions were to improve.

Private-public hybrid: What about EC rentals?

Executive condominiums (ECs) are a public-private housing hybrid product that has proven to be very popular with Singaporeans, as they offer a private condominium lifestyle at a lower cost. However, like HDB flats, ECs cannot be bought to let. Homeowners will need to fulfil a five-year minimum occupation period (MOP) before they can lease out their entire unit.

Rental volumes for ECs have crept up over the period of analysis, with 2014 seeing a 6.7 percent increase in rental volumes over 2013 (refer to Figure 6). The second and third quarters of the year are an active period for rentals, with the majority of transactions taking place then. Rental volumes for ECs are crawling upwards, as their lower pricing, larger sizes and proximity to suburban amenities like schools make them an attractive prospect for expatriate families. ECs are also likely absorbing some rental demand from their private market counterparts, as shrinking expatriate packages are shifting tenants out of the city centre and city fringe, to the OCR where ECs are located.

While ECs are seeing relatively decent volumes, prices have been on a decline. From their recent peak in Q1 2013, average EC rental prices have fallen 13 percent to $2.40 psf per month, a trend reflected in the overall residential rental market. While the decline in prices is worrisome, it is less of an issue for EC landlords than their private counterparts. Due to the MOP and a lack of EC launches from 2005 to 2010, EC rentals hitting the market right now are likely to be older units that were bought at lower prices. EC landlords are therefore likely to be in a much better position to weather market conditions than their private counterparts.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||