With numerous HDB resale flats going for close to and even over a million dollars in recent years, alongside the generally higher cost of housing in Singapore today, aspiring homeowners have been given due cause for concern. But just how affordable is public housing in Singapore?

By Romesh Navaratnarajah and Cheryl Marie Tay

A 5-room HDB resale flat in Toa Payoh made headlines recently after being sold for an astounding $955,000, but that price pales in comparison to the eight other resale flats sold at $1 million or above in Q1 2015, according to HDB data.

In contrast, only two HDB units broke the million-dollar mark for the whole of last year. The spike in such sky-high transactions has been attributed to the Pinnacle@Duxton achieving its five-year Minimum Occupation Period (MOP) last December.

Although industry experts insist such record-breaking deals are the exception and not the norm, many Singaporeans are worried this could mean rising resale flat prices.

Much ado about nothing?

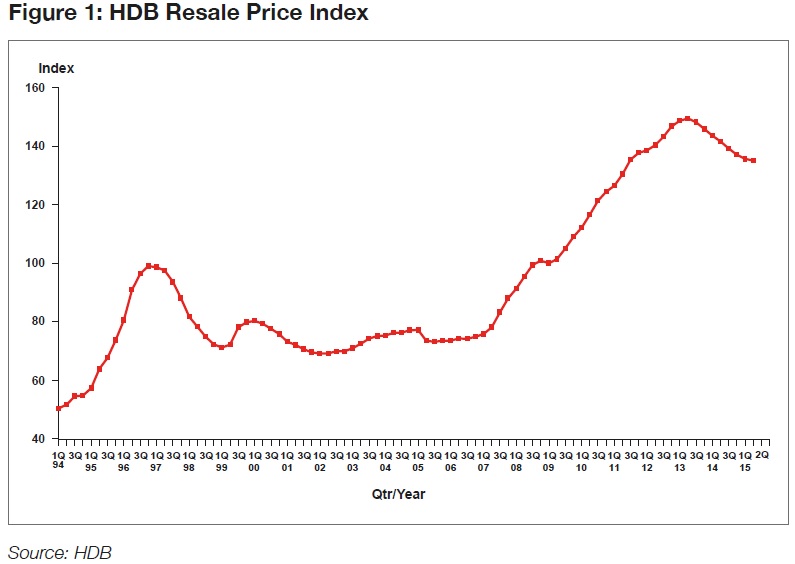

But their concerns may be unwarranted, as the HDB Resale Price Index has been slipping in the last two years. Latest data shows resale prices dipped 0.4 percent in Q2 2015 after falling 1.0 percent in Q1 (refer to Figure 1).

Analysts point to a series of cooling measures introduced by the authorities since 2013, which have brought down skyrocketing flat prices.

“The falling resale prices are due to the potent combination of the government’s measures to stabilise the public housing market, such as reducing the Mortgage Servicing Ratio (MSR) cap of 30 percent and maximum loan term of 25 years for HDB mortgage loans, the three-year wait for new PRs before they can buy resale HDB flats, and allowing singles to buy two-room Build-To-Order (BTO) flats in non-mature estates,” said PropNex Realty chief executive officer Mohamed Ismail.

ERA Realty key executive officer Eugene Lim said the tighter rules on mortgages in the resale market “have effectively restricted the maximum loan quantum a buyer can qualify for, therefore restricting his purchasing power. Buyers can no longer offer high prices”.

“Another measure the government came up with was to do away with the Cash-Over-Valuation (COV). Forcing the buyer and seller to agree on a price before the valuation report can be obtained has resulted in more rational behaviour on the part of both parties.”

While the decline in resale prices may seem small, Lim reckons the measures are sufficient, as prices have generally stabilised in the market.

“The government apparently thinks so as well, as there has not been a new measure introduced in a long while. If any more measures are taken to accelerate the decrease in prices, this might have the unintended effect of crashing the market, which is not ideal,” he said, adding that prices are likely to drop further by as much as five percent for the whole year.

More houses, more prices

Meanwhile, the ramp-up in new flat supply to almost 100,000 units in four years has also helped to relieve pressure on the resale market.

“The HDB has cleared much of the backlog of housing demand, and drawn away buyers from the resale market,” said Lim.

This year alone, some 13,426 flats were launched for sale, of which 8,039 were BTOs and 5,387 were balance flats. The HDB will release about 4,860 flats in Punggol Northshore and Bidadari in November, while another 4,000 flats will be offered in a concurrent Sale of Balance Flats (SBF) exercise.

Lim explained that prices of new flats are delinked from resale prices. “HDB has been selling new flats priced within the affordability of the household income ceiling. The buyer basically needs to right-size the flat he wishes to purchase, based on his income. Also, locational attributes account for the price differential amongst the various flats offered. Those in mature estates are pricier than those in non-mature estates.”

In the last BTO exercise in May, selling prices of 2- to 5-room flats ranged between $15,000 and $354,000, inclusive of housing grants.

Such grants are also available for eligible first-time buyers looking to purchase HDB flats from the open market. “There is the family grant of $30,000, Additional Housing Grant (an additional grant given to those who qualify for the Family Grant) ranging from $5,000 to $40,000 (for families with household incomes of $5,000 and below), as well as the Proximity Housing Grant (PHG) of $20,000, for buying a flat within 2km of or in the same estate as your parents’ home,” said Lim.

Scale model of new flats in Punggol. (Photo: Cheryl Marie Tay)

Assurance of affordability

Regarding the recent introduction of new housing policies such as the PHG and raised income ceiling for more buyers to take out an HDB loan and CPF Housing Grant, Lim does not think sellers are in the position to take advantage of this to increase prices, as buyers nowadays are more prudent in their price negotiation.

“Most will make an offer based on recent transacted prices, and as such, we do not see any huge impact on HDB resale prices being increased as a result of more help from the government.”

It’s no surprise, then, that public housing in Singapore remains the most affordable housing option, with around 80 percent of the population living in HDB flats. To give an idea, the average annual household income for Singapore was $94,440 at the end of 2014, which is 21 percent of an average 4-room resale flat in Ang Mo Kio. In his National Day Rally speech last month, PM Lee Hsien Loong even showed an example of how a household earning below $1,000 a month can still afford a 2-room BTO flat.

According to Lim, “The main aim of the government, when it comes to housing affordability, has always been to provide a range of choices for the public, making sure that almost everyone will be

able to afford at least a house. If a household so chooses to purchase a more expensive unit instead of one that is cheaper but that would serve them equally well, then it is no longer a question about affordability.”

As for resale transaction volume, he expects to see an increase in the coming months, as the new housing policies announced during the National Day Rally take effect, possibly hitting 19,000 to 21,000 units for the whole year.

Ismail predicts a similar resale volume of 19,000 to 20,000 units due to lower asking prices, up from 17,318 transactions last year.

“In particular, the PHG is expected to boost the number of resale transactions, especially in mature estates, as families make use of this grant to purchase a flat near their parents,” added Lim.

Two sides to every storey

But for all this assurance of HDB affordability on the part of property experts and the government, what do homeowners really think?

Web developer Roger Tan, 37, whose monthly income was below $3,500 at the time, paid around $360,000 on the open market for a three-room resale flat in West Coast two years ago. Tan, who is single and intends to live in his home for good, says: “(HDB flats are) affordable, yes. Cheap, no. Affordability is largely dependent on current expenditure and income. On a no-frills lifestyle, this is eminently doable. If you need a Starbucks fix once a day, will die without a set of wheels, will develop cabin fever without a twice-yearly vacation in Europe, and must have new furniture, fittings and air-conditioning in order to go on living, then probably not.”

On the other hand, senior programme administrator Lawrence Chong, 57, who also owns a three-room open-market resale flat, feels HDB flats in general are getting less affordable. Earning a monthly salary of $2,400 at the time, he bought his home in Yuhua in 1994 (at the age of 35) for $94,000, slightly over a quarter what Tan paid for his flat. The comparably low price of Chong’s flat then, combined with the rental income from leasing out one of its rooms, meant it was “practically free”.

Nowadays, he thinks “HDB prices have gone out of control. By 2003, a three-room flat in Bukit Batok was going for $128,000. In 2013, the same flat could be sold for $310,000. This in turn affects BTO prices. It might still be affordable, but you would have almost no CPF left after paying off the mortgage.”

A unique situation

Ultimately, one could say affordability is relative. To a single person aged 35 and above and earning around $10,000 a month, even a 5-room resale flat in a mature estate could be well within his means.

But a couple with young children, even with government grants for BTO buyers, may find it significantly less affordable if their combined monthly income is about $8,000. After all, children’s education and healthcare in Singapore are anything but cheap.

It is worth noting that Singapore has a different definition of “public housing” from other countries. Elsewhere, public housing is usually meant for lower-income households who cannot afford private apartments and houses. Here, 80 percent of the population, from lower-income to even upper-middle income types, live in HDB flats, which were originally built to provide affordable homes for Singaporeans.

Recently, however, Minister of State for National Development Dr Maliki Osman said that Singapore’s public housing policies are not only about meeting basic needs, but also “fulfilling aspirations”. Given that a 3-room BTO in a non-mature estate already costs upwards of $150,000, it’s not hard to make the connection.

It might be slightly puzzling — or worrying, even — that public housing is to be considered an “aspiration”, even as sizes shrink and prices sometimes increase.

Still, the cooling measures introduced to stabilize the residential market have proven effective in reducing flat prices, and one can only hope this continues to be the case, so more Singaporeans can afford their own homes.

| This article was first published in the print version The PropertyGuru News & Views. Download PDF of full print issues or read more stories now! | |||