It’s time to take a look back on how the real estate market performed in 2015. Although there are some early signs of recovery, sellers should not be rejoicing yet.

By Chang Hui Chew

Another year has passed, but for those in the real estate industry, it has been a long year with few bright sparks. Cooling measures have slowly but surely brought down prices, even as transaction volumes are seeing signs of recovery.

It is possible that both sellers and buyers have come to accept this new normal. We have seen developers start to “right-price” across all segments, helped by the fact that most of the new launches hitting the market saw their land sales taking place after the implementation of cooling measures, so the land bids were more cautious. Likewise, many of those looking for a home might have felt that the overall quantums had fallen to a level that were acceptable for their wallets.

In 2015, the key driver for property transactions remains affordability. The segment is price sensitive, and buyers are motivated by good deals.

Private non-landed property

The non-landed private property market remains lukewarm at best, with over 12,400 transactions caveated in 2015 (refer to Figure 1), an 8.6 percent improvement from 2014’s 11,400-plus transactions. This worked out to be about an average of 1,000-plus units cleared per month, with an overall median price of $1,230 psf.

Flash estimates by the Urban Redevelopment Authority (URA) show that overall prices fell by 3.7 percent in 2015, a slight slowdown in declines compared to 2014’s 4.0 percent. Speculation and short-term flipping have practically fallen off the radar for this property segment, with sub-sales 3.7 percent of total transactions in the year. 56.5 percent of all transactions were new sales, and 40.1 percent were resales.

Right-pricing properties, more than ever, becomes imperative for developers to move properties in an environment where Total Debt Servicing Ratio (TDSR) has constricted liquidity and stamp duties have increased the cost of ownership. CEL Development’s High Park Residences was the clear winner in the private non-residential market in 2015, with 1,105 caveats for the project lodged in the month of July alone, at a median PSF of $1,016. Recorded prices for the project started around $373K for a studio unit, which suggests that capital outlays started at around $74K, a palatable amount for most investors.

To reach this price point however, some compromises were made. The average size of units sold in High Park Residences was around 788 sq ft, which could be a tight squeeze for families with children. This appears to be a trade-off many buyers were willing to make, with the project close to sold out at time of writing, and studios and one-bedroom units fully sold out.

When we look at the top five projects sold in 2015, it is clear that aside from pricing, location is the other common factor. Out of the top five, three are located in the Rest of Central Region (RCR), suggesting that drops in pricing have made it more feasible for buyers to move from the outskirts to locations closer to the city. While Frasers’ North Park Residences is further out than the other projects, it is a massive integrated development and brings huge conveniences to its residents.

Furthermore, all five projects are located within walking distance to MRT or LRT stations, which also increases their value proposition for homebuyers. On the ground, we also see several new launches that are not within close proximity to MRT stations offer shuttle bus rides to the nearest MRT station for residents, to compensate for this.

Executive Condominiums (EC)

This public-private hybrid property class saw some excitement in 2015, with the Prime Minster announcing an increase of the income ceiling from $12,000 to $14,000 during the National Day Rally. This allowed many couples and families who felt that they were part of the “sandwich class” – those who earned too much to buy Build to Order (BTO) flats or ECs, yet found themselves having to stretch financially to pay for private property – a viable option for home purchases.

At the same time, a proliferation of EC land sales by the state in the past couple of years, especially in the North and Northeast regions of Singapore, not only meant that buyers had a variety of projects to choose from, but that developers also had to price even more competitively to attract buyers.

Over the course of 2015, 3,310 EC units saw caveats lodged, with an overall median price of $793 psf (refer to Figure 3). By transactions, MCL Land’s Sol Acres had the best market performance, with 371 caveats recorded, at a median of a rather affordable $788 psf.

Some of the most popular projects for 2015 were not the latest launches (refer to Figure 4). The Terrace, Bellewaters and Bellewoods saw marketing starts in 2014, but their popularity in the past year was likely due to the developer offering attractive rebates and discounts to buyers. Again, right-pricing here, especially in areas where there is plenty of competition for ECs, helped developers move stock.

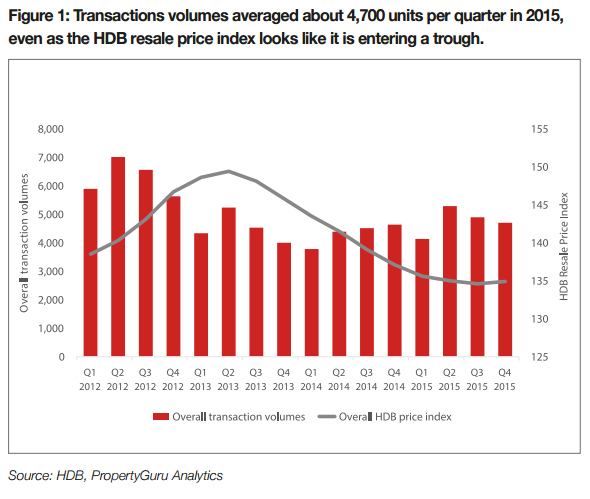

HDB Resale

After falling for nine consecutive quarters, prices for resale flats rose by a conservative 0.2 percent in the last quarter of 2015. While overall prices did still dip 1.5 percent from the previous year, the decline has slowed, compared to 2014’s 6.2 percent fall in prices. 2015 saw over 17,800 HDB resale transactions, an increase of 10.6 percent from those in 2014. However, market watchers are cautious to declare this a recovery, and we will likely have to see a few more quarters of modest price increases before we can declare that the HDB market is out of the doldrums.

Figure 5 shows HDB resale price and volume trends by estate. A trend that emerges from the data is that estates with a larger volume of transactions also tend to be the ones that are priced a lot more affordably. Like all the other market segments hence, pricing, and indeed, right-pricing are key. A couple of the bigger mature estates with established amenities, like Tampines and Bedok, moved well in 2015, at a median of $401 psf and $423 psf respectively. Scarcity continues to drive higher prices, with resale flats in Bishan, Marine Parade, Bukit Timah and the Central Area continuing to command higher prices.

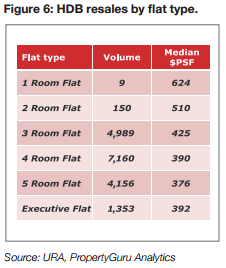

40 percent of the flats sold in 2015 were four-room flats, which remain popular starter homes with adequate space for a family of four. Executive flats, which include maisonettes and jumbo flats, comprised 7.6 percent of resale stock sold last year. Five-room flats had the lowest median psf price overall at $376 psf, 4.2 percent lower than executive flats, which went for a median of $392 psf.

Pinnacle at Duxton made headlines in 2015 for record-breaking sales, including the record for a four-bedroom flat at $990,000. According to the data, 122 units moved at Pinnacle, of which 90 were four-room flat units. The lowest priced resale unit sold at Pinnacle was a low-floor four-bedroom unit, which moved at $650,000, a relative bargain, while only nine units moved above the million-dollar mark.

Retrospective round-up

The general consensus is that we will begin to see a recovery in 2016 in the property-for-sale market, with 2015 and perhaps the first half of 2016 the trough of our current property cycle. However, developers and sellers need to be wary of being overly optimistic.

Signs of recovery are weak, and the real estate segment remains extremely price sensitive. Coupled with the fact that affordability is unlikely to increase further with the government stating on record that the TDSR is here to stay, sellers could easily alienate buyers by rushing to increase prices.

| This article was first published in the print version PropertyGuru News & Views. Download PDFs of full print issues or read more stories now! |

|||