Singapore’s residential market has seen transaction volumes pick up, but prices continue to decline, or remain stagnant.

In this issue of the Guru View, we take a look back at the HDB and the non-landed private residential market, to understand how the market has moved.

by Chang Hui Chew

Every year, as the Christmas decorations go up in Orchard Road, it reminds us that another annual cycle is coming to an end. And what a year 2016 has been

Globally, we have seen changes we could not have predicted at the beginning of the year. In June, the United Kingdom voted to leave the European Union by referendum, putting the future of the common market into question. Earlier in November, the United States saw the controversial election of Donald Trump as president, putting international treaties like the Trans-Pacific Partnership (TPP) and the Paris climate agreement at risk of failure, sending shockwaves across markets internationally.

Closer to home, the 1MDB saga rocked our northern neighbour, with the fallout hitting Singapore-based financial firms like Falcon Bank, who were embroiled in the scandal. In the second half of the year, oil and marine based company Swiber Holdings suddenly collapsed, a sign that protracted declines in oil prices might significantly affect our local economy.

2016 might therefore best be described as a bit of a roller-coaster ride, with those of us watching the markets, including the property market, trying to anticipate the next hurdle. At the same time, with real estate often perceived as a safe haven asset, especially in Singapore, does it not stand to reason that the real estate market might have benefitted in some form from the events of 2016?

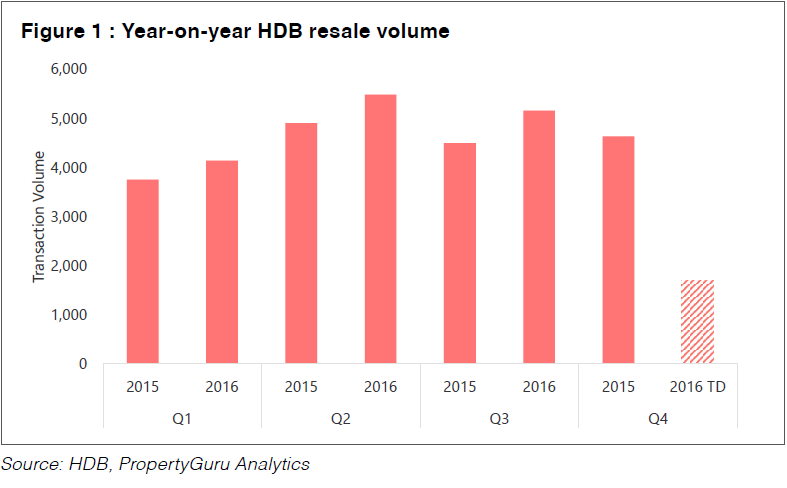

HDB resale market

In 2016, the HDB resale market has seen volumes increase over the sector’s performance the year before (refer to Figure 1). Of note was Q3 of this year, which saw an almost 15 percent increase year-on-year (YOY) over the same period in 2015.

This should come as welcome news to many HDB upgraders, who need to offload their existing HDB flats, before moving on to a larger HDB flat, or to private property. The increase in transactions suggests that demand has picked up in the HDB resale market, with buyers accepting that cooling measures, such as the Mortgage Servicing Ratio (MSR) for HDB purchases, is here to stay.

The MSR mandates that borrowers are not able to use more than 30 percent of their gross monthly income to service their HDB home loans, regardless of whether the loan was taken from HDB or through a bank. Together with the abolishment of cash-over-valuation, HDB resale prices saw declines in 2015, then remained flat in 2016.

Between Q1 and Q3 of 2016, the HDB resale price index stayed at 134.7. This suggests that prices are at somewhat of an equilibrium at the moment, with buyers likely made cautious by the cooling measures, and by the prospect of a global economic slowdown.

Given the macroeconomic headwinds however, it is unlikely that we will see Q4’s volumes exceed 2015’s, and we will likely see HDB resale prices continue to remain flat or decline.

Another trend that we have seen emerge in 2016 is the increase of HDB flats selling at sky-high prices. In 2013 and 2014, we saw less than 20 HDB resale units transact above $950,000 per year. In 2015, this number shot up to 51. This year, 63 units have transacted at these prices by time of writing in mid-November (refer to Figure 2).

As we mentioned in a previous Guru View, to put it in context, this number remains a tiny fraction – 0.4 percent – of all the HDB resale units that exchanged hands this year. Yet, the increase in these expensive flats grab headlines and the frequency at which it is reported has seen sharp rises as well.

Prior to 2015, the majority of these expensive flats were older, rarer unit types in smaller mature estates, such as maisonettes in Bishan. Starting in 2015 however, we begin to see centrally located flats, such as the Pinnacle @ Duxton, and this year, City View @ Boon Keng, transact at these prices. Aside from their location, their unique designs also add to their value, incentivising those with the means to offer such prices.

Private residential property

Like its public counterpart, non-landed private properties have seen volumes climb against 2015’s numbers YOY (refer to Figure 3), providing hope to sellers who not been able to offload their units.

Q3 2016 saw the most number of units moved this year, with over 4,000 caveats lodged, on the back of the stellar performance of a number of new launches. MCL Land’s Lake Grande moved over 500 units in the quarter alone, a bright spark in what has been a rather lacklustre property market, on the back of the Jurong Lake District’s growth story and attractive pricing.

A number of other new launches also did relatively well, including Poiz Residences, Kingsford Hillview Peak and Sturdee Residences, to name a few. Of particular note is Cairnhill Nine, a prime property located in the prime Orchard Belt, which saw units snapped up at launch, and at time of writing, is more than three-quarters sold.

Cairnhill Nine’s performance bucked a market trend which saw movements in prime properties come close to a standstill, between cooling measures and the attractiveness of prime supply in other safe haven markets like Tokyo and Sydney. Most market watchers agree that Cairnhill Nine’s strong sales were due to a strong product offering, with access to Paragon Medical Centre, and its location in the Orchard belt.

A number of projects that recently completed construction or are close to completion also saw greater interest in 2016, with developers offering schemes, such as deferred payments, to help sweeten the deal for buyers.

While unit take up has been encouraging for developers, private sellers have been seeing increased interest in their segment as well.

The third quarter of 2016 also saw a whopping 42 percent increase in non-landed private property resale volume over the same period in 2015. Interestingly, while private property purchasers with HDB addresses grew by 28.6 percent in the quarter YOY, those with private property addresses grew by over 51 percent.

This suggests that while HDB upgraders are still actively looking at the private property market, buyers already living in condominiums are more aggressively either looking for investment properties, or moving to another unit in the same property class.

Similar to what we saw in the HDB resale market, while volumes have moved upwards, prices continued to edge downwards as well. The third quarter of 2016 marked the 12th consecutive quarter of price declines, according to the Urban Redevelopment Authority’s (URA) non-landed residential price index (refer to Figure 4).

These price declines reflect an overarching narrative of a real estate market going through a period of correction, with home buyers made far more cautious due to restricted affordability and the expectation of lower prices. For upgraders, lower prices also imply that they are not able to cash out of their existing units at higher price points, thus limiting offers for their next home.

At the same time, current new launches to the market have somewhat of an advantage over projects that launched earlier. Land bids post-implementation of cooling measures have been a lot more conservative, reducing developer break-even pricing. Furthermore, developers for new launches are also entering the market with pricing strategies geared towards lowering overall quantums to match reduced buyer appetites.

Rounding it up

As we end the year, it seems that 2016 was a period of right-pricing – market demand picked up on the back of falling prices, as sellers began to price closer to buyer expectations. The increase in transaction volumes for both HDB resales and private non-landed property is encouraging, as it implies that buyers have started to dip their toes into the market again.

Singapore buyers remain highly price sensitive as affordability is a huge issue. While we constantly hear rumblings from real estate professionals calling for a tweak to the cooling measures, the state has constantly reiterated that measures like the Total Debt Servicing Ratio (TDSR) are here to stay. It took a while, but it seems that the market has accepted these regulations as the new normal.

| This article was first published in the print version PropertyGuru News & Views. Download PDFs of full print issues or read more stories now! | |||